Prequisites

To use this strategy you should have available the following prequisites

- Quantower trading platform . Click to Download the platform

- Free Quantower License. Click Here to get one

- automated-trading.ch Account with Premium Subscription

- Futures or Crypto Account to get the Data (CQG, Rithmic or Tradovate, Binance, ByBit....)

We highly recommend joining our discord community by following this invite link

![]()

Important Disclaimer

We strongly recommend that you never run your algorithmic trading systems on your hard-earned real money. You should always minimize your risk and run your strategies on trader funding programs so that the maximum amount your risk to lose is the monthly subscription fee you pay those programs.

Here are the trader funding programs that we recommend using, and that we use to run this Opening Range Breakout strategy on:

- Lucid Trading

- Funded Next

- Tradeify

- Apex Trader Funding

- Want to know more about propfirms and how to chose the best one ? Click Here

Description

The Opening Range Breakout strategy is based on entering on a signal generated by analyzing market behaviour in regard to a price range formed around the first minutes of the trading session. The strategy provides a very flexible entry setup based on that breakout concept

The strategy will start by detecting the opening range, the opening range is a range defined as a an interval that can be parametrized, but in general terms the opening range should be located around the opening market hour of 09:30 EST for most of the future market instruments. The opening range can, for example, be defined between 09:30 EST and 09:35 EST (spanning 5 Minutes) or from what is know as Cash Open from 08:30 EST to 09:30 EST. One should experiment with different intervals and seek the most adapted interval for each instrument.

For Crypto markets, the opening of a session is irrelevant since crypto markets are always open even on weekends. But since there is a strong correlation between crypto instruments and US market futures one can use US market session intervals to define the opening range interval for crypto markets

The second step of the strategy is to wait for a breakout of the price from the opening range. The strategy will wait for the price to retest the range as the first required condition before deciding to open a trade. After the retest, the strategy will wait for the price action to show a strong breakout in the direction of the initial retest. Precisely, the strategy will look for a Faire Value Gap that will be the trigger to enter a trade, or the strategy can be set to an immediate mode which will enter trade at the close of a bar without waiting for Faire Value Gap to occur. Also the strategy will look for these entry conditions to occur before a certain time limit for the day. Generally speaking, the more you wait for the price to breakout the more the price can get far away from the initial price range, so I put a time limit to 11:00 EST for example, meaning no trades will be allowed to be triggered after 11:00 EST. Off course this is a parameter that you can modify.

Entering a trade is an important part for any strategy, bu what is more important is managing the trade. The strategy allows to manage the trade with many management methods.

Along with the initial setting of the Stop Loss price, a Take Profit price and a dynamically set Quantity to maintain a Fixed Risk per trade which is a crucial part of any strategy

profitability on the long run.

The Stop Loss price can be set to Fibonacci levels calculated on the retracement on the opening range zone.

All these steps are configurable and can be enabled/disabled which makes this strategy very lenient and adaptable to a wide range of scenarios

Entry Setup Examples

One drawback of Quantower on comparison of other platforms such as Ninjatrader, is that a Quantower strategy cannot draw on the Chart, only indicators can. Meaning that the strategy will analyze the opening range without being able to draw it on the chart for us to visualize it. For this reason, I will draw on the chart myself to demonstrate some examples.

Example #1: Perfect Entry Setup on MES

On this example entry setup which is run on MES on the 1 Minute Timeframe, the opening range is set to span from 09:30 to 09:45 EST. And a Faire Value Gap is required for entering a trade after price retrace to the opening range, with stoploss set to the supertrend level at the entry time. The time on the chart is UTC+1, this is why the opening range appears on 15:30 (chart time) instead of 9:30 (EST)

After the opening range has finished forming, you can notice on the example that the price broke down from the range at the bar marked 2.. This marks the first event required for the strategy to enter a trade.

After this step, the strategy will wait for the prie to retrace back to the opening range. The retracement can be triggered by any tick that goes inside the opening range, which occured at the candle marked with 3.. This event marks the second required condition for a valid entry setup. After that the strategy will be armed for entry and it will wait for an FVG to trigger the entry which occured at the 3 candles marked with 4.

The stoploss can be calculated according to multiple options. The chosen option on this example is the Supertrend indicator which has set the stoploss price to the supertrend DownTrend line. The take profit was set according to a 2:1 calculation leading to a winning trade.

The sequence of this example was the following :

- First breakout from the range (no FVG is required)

- Price retraces back to the range

- Price breakout 2nd time from the range with an FVG (Faire Value Gap)

Entry setup parameters explanations

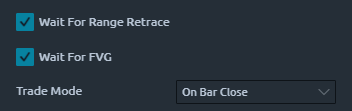

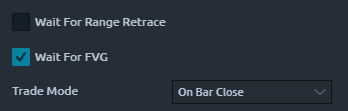

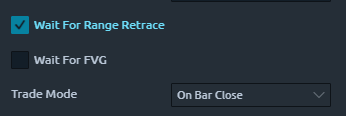

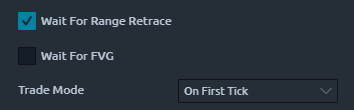

By enabling/disabling certain parameters of the strategy one can change these required steps, here are some examples of the parameter values with their entry setup outcome:

|

This parameter values will require the following sequence :

|

|

This parameter values will require the following sequence :

|

|

This parameter values will require the following sequence :

|

|

This parameter values will require the following sequence :

|

Features

The Opening Range Breakout strategy has a set of unique features:

- No pending orders are placed: only market orders

- Full-auto strategy that can be scaled into multiple instances

- Precise backtesting capabilities based on Tick Level playback to obtain precise entry/exit backtesting executed on tick level

- Robust In-house Order management library. Resistant to connection loss and works seamlessly on Rithmic accounts or other connection

Here I further explain some of the features of the strategy in more details

Futures on US indices or Crypto pairs

The strategy works seamlessly on both US Futures instruments such as ES, MES, NQ, MNQ..., or on crypto futures available on popular crypto exchanges such as ByBit or Binance

Dynamic Quantity and Risk Management

As all our strategies, this strategy implements two methods to set quantity for open positions.

- Fixed Quantity: This method will use the same quantity value for each position. If the stoploss is variable between positions (by using a dynamic stop loss value), The win/loss will be also variable between positions

- Dynamic Risk Adjusted Quantity: This method will calculate quantity of each position based on multiple factors:

- The stoploss of the position

- The maximum risk (in $ currency value) allowed for a position to take

- The maximum quantity allowed for a position to take

Position Management

As all our strategies, this strategy implements mutiple position management methods :

- Classical Trailing Stop:This method will trail the stop loss of the position based on a trigger and a trailing amount

- SuperTrend indicator:This method will manage the position based on the SuperTrend indicator

Apart from those position management methods, the strategy allows to set the stop loss based on multiple strategies and to set the take profit based on different ratio based methods. Check the parameters section for a detailed explanation

Account Management

The strategy implements daily stop-trading triggers based on the Net winning position count, the Net losing position count or when a target realized Net profit is reached. or when a target net loss is reached.

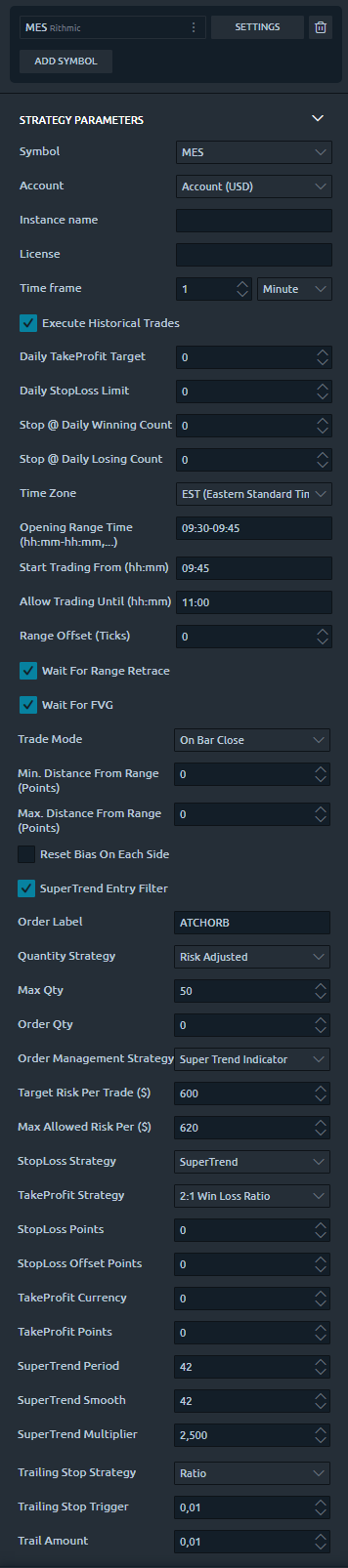

Parameters

We try to keep the parameters to minimum. We only left the most important parameters to be set

| General | |

| Execute Historical Trades | This parameter is very important and should be used carefully. This parameter will enable executing trades when the strategy is run on Historical mode you may check this parameter to test the performance of the strategy on days in the past or to simply test if the used parameters will generate trades on the current day. But when you run the strategy on Live mode, you should uncheck this parameter. |

| Daily TakeProfit Target | The strategy will stop when the daily TakeProfit amount is reached after a position is closed. When set to 0, this parameter is ignored |

| Daily StopLoss Limit | The strategy will stop when the daily StopLoss amount is reached after a position is closed. The value of this parameter is positive. For example if the value is set to 300, the strategy will stop when the Realized PnL is lower or equal to -300$. When set to 0, this parameter is ignored |

| Stop @ Daily Winning Count | This will make the strategy stop trading if the net count of winning trades for the day is equal to the value of this parameter. This parameter is ignored if equal to 0 |

| Stop @ Daily Losing Count | This will make the strategy stop trading if the net count of losing trades for the day is equal to the value of this parameter. This parameter is ignored if equal to 0 |

| Entry Setup | |

| Time Zone |

This parameter sets the time zone to be used for setting the Trade Time parameter below. Since futures markets are open and closed based on US market time zone which is EST (US Eastern, New York), this parameter allows you to specifiy trade time interval on another timezone which is your local machine timezone

|

| Open Range Time (hh:mm-hh:mm,...) | This sets the opening range interval. Example : 09:30-09:35 will define an opening range spanning from nine-thirty to nine-thirty-five AM. The tim zone is specified by the previous parameter. After this interval is finished, the range will be drawn in the chart marking the its high and low prices |

| Start Trading From (hh:mm) | This parameter sets when the trading should start after the opening range has started. In most cases you would want trading to start as soon as the opening range has formed, but sometimes you would want to wait some time before the strategy starts trading. |

| Allow Trading Until (hh:mm) | This parameter sets when the trading should stop after the opening range has formed. This time will restrict new trades to be open but will not affect already open positions to be managed. |

| Range Offset (Ticks) | This parameter sets adds an offset in ticks to the calculated opening range. The offset is added to the high price and to the low price of the range. For eample if you set the value of this parameter to 4 Ticks, the opening range will be extends by 4 ticks to the top and by 4 ticks to the bottom. |

| Wait For Range Retrace |

This option will make the strategy wait for the following sequence of events before entering the trade:

|

| Wait For FVG | This option will make the strategy wait for a valid Fair Value Gap while breaking from the range. The FVG can occur after the breakoff. When this option is not used, the strategy will only wait for a bar close in the direction of the trade |

| Trade Mode | This parameter sets the entry mode after a retest of the Opening Range zone

|

| Min. Distance From Range (Points) | this parameter will set the minimum required distance in points from the range to the current price in order to trigger a trade. If you set this to the value 0, it means as soon as the price break from the range, the strategy can trigger a trade. If you set this to for example 4 points, the strategy will not open a trade until the price break from the range for at least 4 points |

| Max. Distance From Range (Points) | this parameter will set the maximum allowed distance in points from the range to the current price in order to trigger a trade. If you set this to the value 0, it means no control on the distance is made. If you set this to for example 10 points, the strategy will not open a trade until if the price break from the range for more than 10 points from the range upper or lower level |

| Reset Bias On Each Side | This parameter is only used when the Wait For Range Retrace is enabled. This parameter will have the following behaviour:

|

| SuperTrend Entry Filter | This parameter will enable/disable using the SuperTrend indicator as an entry filter. When this is enabled, Long trades are allowed to enter only when the SuperTrend is in bullish mode. Inversly, it allows short trades to enter only when the SuperTrend indicator is in bearish mode. Notice that this will result in fewer trades overall |

| Order Label | The parameter will let you set a Label that will be suffixed to all positions sent to the broker. This is useful in case you want the positions sent to the broker to have a specific value to differentiate them from positions of other people using the same strategy |

| Quantity Strategy |

This parameter sets how the quantity should be set for a Trade

|

| Max Qty | This parameter sets the maximum allowed quantity when the Risk Adjusted method is selected. This option is very useful since some propfirms has order quantity limits that can cause the account to be invalidated |

| Order Qty | This parameter is only used if the Quantity Strategy is set to Fixed. This parameter sets a fixed quantity of each trade. In the case of increasing orders quantity executed by the order management mechansim, this parameter is also used for each increase in quantity. Generally, We would use the values 1 or 2 for this parameter |

| Order Management | |

| Order Management Strategy |

|

| Target Risk Per Trade ($) | This sets the max risk in dollars for one position.

|

| Max Allowed Risk Per ($) |

|

| StopLoss Strategy |

|

| TakeProfit Strategy |

|

| Stop Loss Points | This parameter is available if the Stop Loss strategy is set to Points |

| Stoploss offset Points | This parameter will add an offset of points to the calculated stoploss level. This offset will be used when calculating Risk per trade |

| Take Profit Currency | This sets the take profit in dollars for the open position. If you use the Fixed Currency Value as a take profit strategy, the value of this parameter will be used. If not, make sure to set this parameter to a high value to not interfer with other ratio based strategies |

| Super Trend | |

| SuperTrend Period | This sets the supertrend period |

| SuperTrend Smooth | This sets the smoothing period of the supertrend |

| SuperTrend Multiplier | This sets the Supertrend multiplier. The bigger this parameter the wider the supertrend bands |

| Trailing Stop Parameters | |

| Trailing Stop Strategy | When the Classic Trail Stop method is selected, this parameter let you chose on which basis the trailing will be calculated

|

| Trailing Stop Trigger | When the Classic Trail Stop method is selected, this parameter sets the trigger (in Points or in Ratio) |

| Trail Amount | When the Classic Trail Stop method is selected, this parameter sets the amount (in Points or in Ratio) to be trailed when the trigger is hit |

Backtesting and Preferred Settings

Here I will try to periodically list backtests with different risk appetit. But before that here are some remarks regarding backtesting

- Past results are not guarantee of future results. All backtesting results are for indicative purposes only

- The period on which the backtest was run was not handpicked to show the best results, The backtest period is the month prior to the first release of this strategy

- Commissions are included in the backtests to get as realistic results as possible. The commission schema used is the same as Apex trader funding program for US futures, and the same as ByBit for crypto futures

- At automated-trading.ch we run very precise backtests due to the following 2 factors

- We are running backtest on the maximum precision on intrabar granularity by using tick level DataSeries

- We are only using Market Orders instead of Pending Orders, in both real-time and becktest modes.

How to run accurate tick-level backtests on Quantower

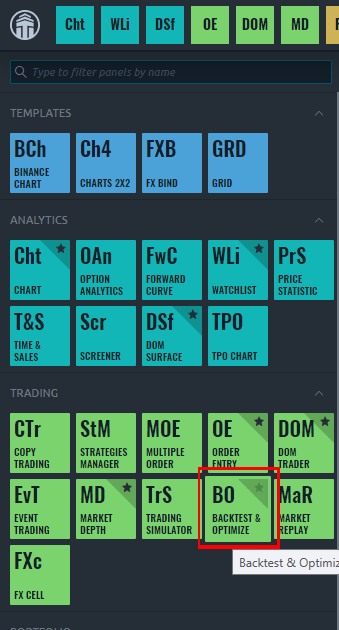

To run backtests on Quantower, first click on the Backtest button as shown on the image below.

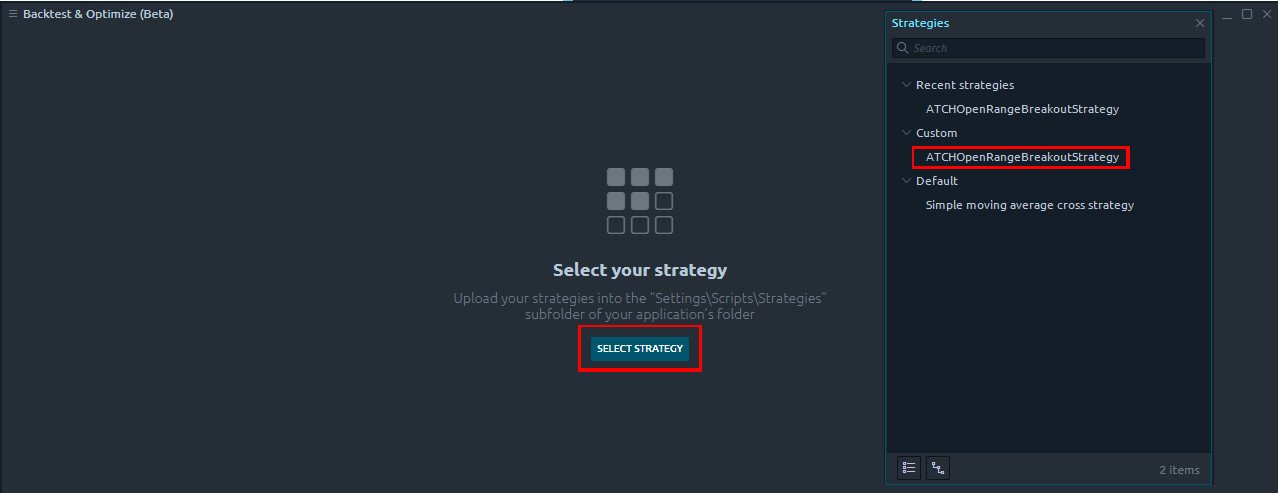

Then you should select the strategy as shown below

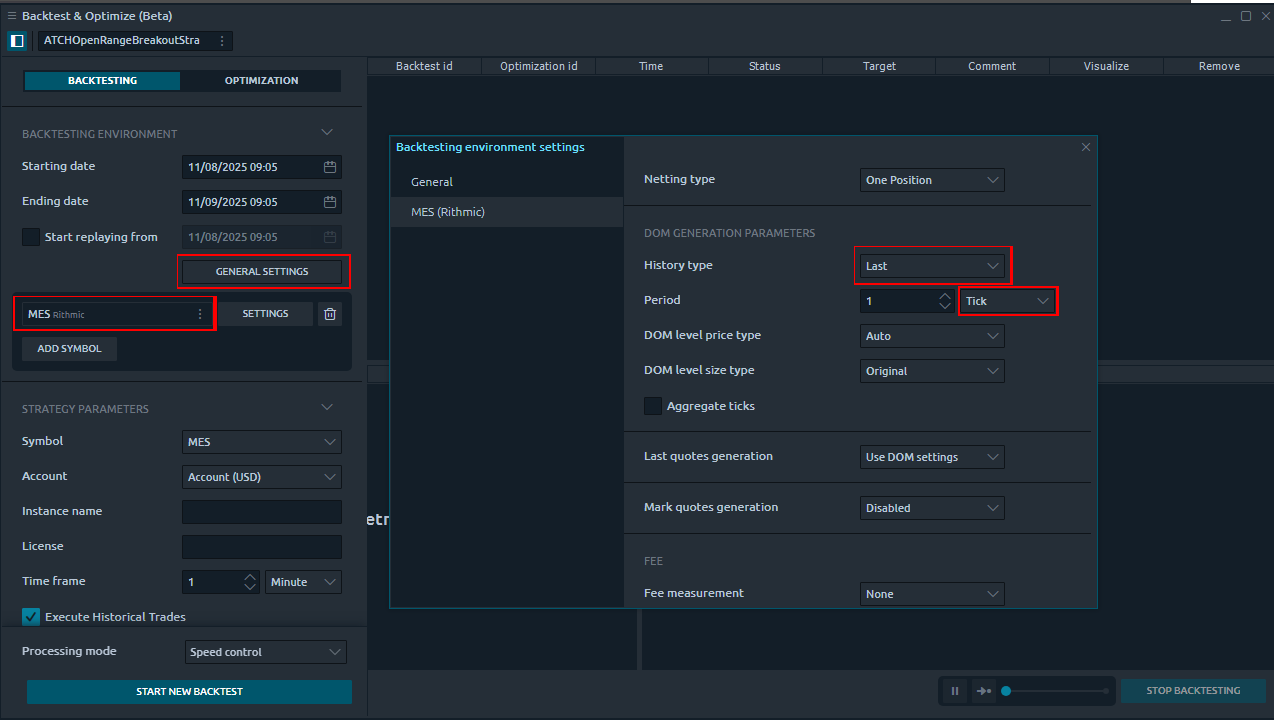

Then, you should select the symbol, in the example below, we have selected MES as Symbol. Once the symbol is selected you should click on the General Settings button. On the window that will open, you should make sure the History Type selected is Last and the Period is Tick

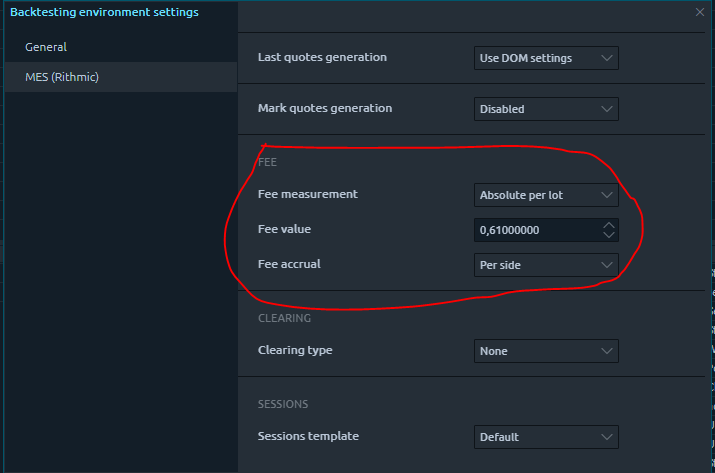

Fees should manually specified. For MES futures you should set the fees to 0.61 like shown on the image below

Backtest results

Here I will try to periodically list backtests with different risk appetit. But before that here are some remarks regarding backtesting

- Past results are not guarantee of future results. All backtesting results are for indicative purposes only

- Commissions are included in the backtests to get as realistic results as possible.

- At automated-trading.ch we run very precise backtests due to the following 2 factors

- We are running backtest on the most accurate data series which is the 1 Tick level data series

- We are only using Market Orders instead of Pending Orders, in both real-time and becktest modes.

- Instrument MES

- Timeframe Minute 1

- Period From 13 March 2024 to 5 September 2025

- Run Mode Backtest

- Total Profit 39 559 $

- Max Drawdown (-3 544) $

- Run Release Version 1.0.0.0

Download & Installation Instructions

To download and install the strategy follow the instructions below

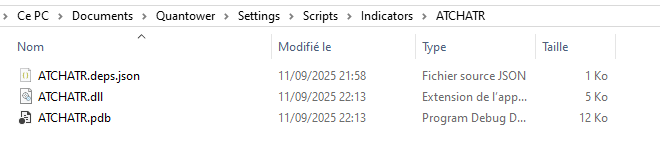

- The strategy requires installing the ATCHATR ATR indicator first. Click on the below button to download the indicator

- As illustrated on the image below, extract the whole content of the zip file into your Quantower indicators folder. The indicators folder can be found by default following this path : {C:\Users\{Windows Username}\Documents}\Quantower\Settings\Scripts\Indicators

- Make sure the files are extracted inside a new folder called ATCHATR

- The strategy also requires installing the ATCHSuperTrend indicator first. Click on the below button to download the indicator

- As illustrated on the image below, extract the whole content of the zip file into your Quantower indicators folder. The indicators folder can be found by default following this path : {C:\Users\{Windows Username}\Documents}\Quantower\Settings\Scripts\Indicators

- Make sure the files are extracted inside a new folder called ATCHSuperTrend

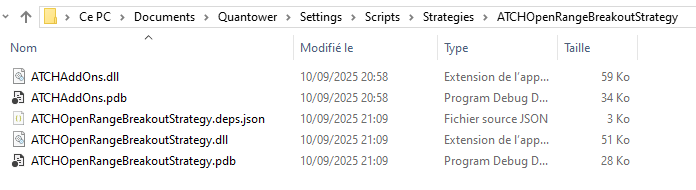

- Once those two indicators are installed, the next step is to download and install the strategy file

- As illustrated on the image below, extract the whole content of the zip file into your Quantower strategies folder. The strategies folder can be found by default following this path : {C:\Users\{Windows Username}\Documents}\Quantower\Settings\Scripts\Strategies

- Make sure the files are extracted inside a new folder called ATCHOpenRangeBreakoutStrategy

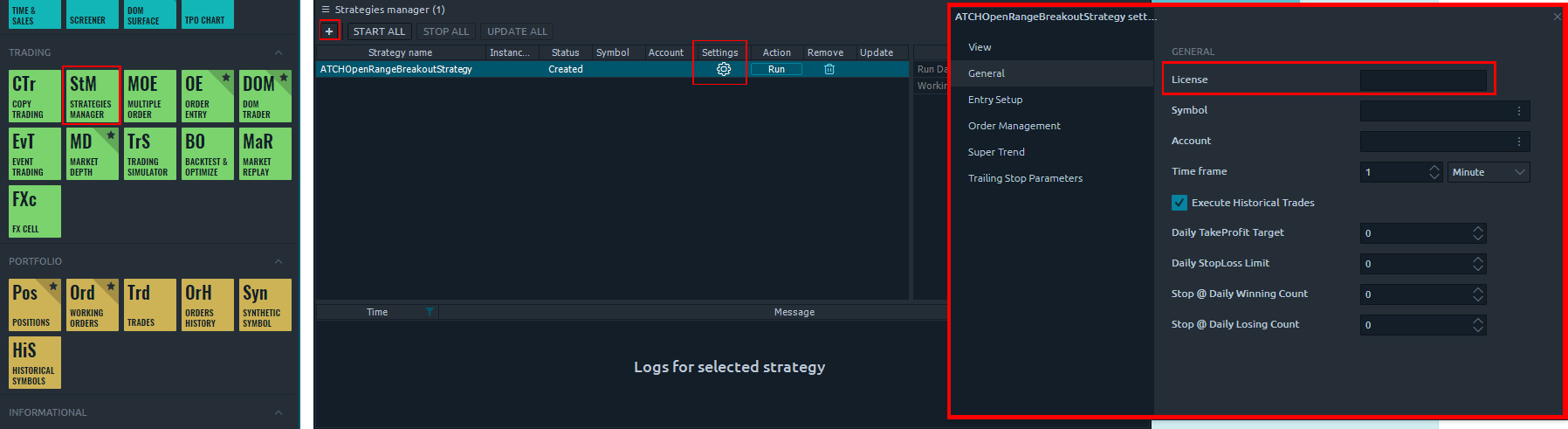

- To start the strategy you should first click on the Strategy Manager module on quantower menu like shown on the image below

- Then Click on the + button to add the strategy. Once added, you should open its settings

- On the settings panel you should enter you automated-trading.ch License that you can get from here billing main page

Frequently Asked Questions

General

Yes! this strategy can run on crypto pair futures such as BTC/USDT future from ByBit

Yes! this strategy can run on weekends when it is used on Crypto futures. When run on US futures it will not run on weekends

Yes! you can use a copier, but a better solution would be to run multiple instances of the strategy. The purchased license allows you to run unlimited instances on multiple machines

Yes! The strategy is designed for that exact purpose. It will work seamlessly on Rithmic, Tradovate, ByBit futures or any other provider connected to your Quantower platform

I designed this strategy to be full-automatic strategy. Yet, it can be used as a semi-auto strategy to enter trades and then let you manage those trades manually using its command buttons

You should consider full auto-trading over manual trading for many reasons:

- Trading 24/7: Automated trading strategies don't need to go to the bathroom not it need to take a break

- Better execution, faster and more precise

- Eliminate psychology and sentiments

- Can be scaled to dozens if not hundreds of instances

- Automated trading can generate truly "passive" income, manual trading is just another "more stressful" job

Yes, If you have an idea that you believe can improve the performance of this strategy, I will be more then happy to hear from you. Please use the contact page to send me a message

No, the source code of the strategy is protected for copyright reasons

Billing

Yes, you can cancel your subscription from the account page at any time to prevent future payments. We cannot refund the unused portion of your subscription, but you will be able to use your subscription even after cancelling for the remainder of the billing cycle.

No, we don't offer a trial subscription plan.

We do not offer full or partial refunds, but you may cancel your subscription at any time to stop future payments.

Skeptics

I have been a professional software developer since 2010. I have been developing automated trading strategies since 2012, for my self for fun and profit and also been developing strategies for clients all over the world

I have always been invlolved professionaly in the business of Finance and Investing, I have worked for trading brokers and investment banking.

I'm not a marketer, and I don't hire someone else to develop my strategies.

I'm not selling it, I'm renting it to generate an additional income and diversify my different sources of income besides what this strategy can generate. Which you should also do. You should not rely on one source of income to reach financial independance, the key is diversification.

The edge of this strategy will not disappear if many people start using it. This strategy is purely mechanical and does not rely on a hidden quantitative pattern that should not be disclosed

Lets examine pros and cons of pending orders

- Pros:

- Best price execution when using limit orders

- Protection against losses in case of connectivity issues

- Cons:

- Can get rejected on high price volatility

- Delay between request to place the order and when it gets placed. Price volatility can cause the order to be rejected and the price to run away

- Requires management: any opposite orders need to be canceled

- Visible to the broker, placed orders can be manipulated

After years of developing strategies I reached the conclusion that market orders are better suited for the context of automated trading.

The main drawback of using pending orders is the fact that they can be rejected which is very hard to manage especially in a volatile environment

In all our strategies, we use market orders even for take profit and stop loss. Lets examine the pros and cons of market orders

- Pros:

- Guarantee of execution reagrdless of volatility conditions

- Invisible to the broker before they get submited

- No risk of being rejected which means better protection for stop loss

- Faster execution than pending orders

- Cons:

- In the case of the connection being lost with the broker, the strategy will be unable to send market orders

We are following the Quantower official guide on how to achieve precise intrabar granularity backtesting by using Tick level DataSeries for execution

Don't take my word for it. Test it yourself, at the end of each trading day, run a backtest of the strategy on that day and compare it with the live trades the strategy made during the day.

Release Notes

- Fix Bug : Error when running multiple instances of the strategy

- Fix bug : Null exception when managing positions

- Fix Bug : Trades open but strategy doesn't detect them because of different instrument name between simulation and real account

- Fix bug : range is finished forming but trade setup is initialized on bar later

- Fix Bug : Setup Closed on each tick making the strategy reset in an infinite loop

- First Release of the strategy

User Comments & Feedback

You can find feedback of our users and ask questions about this strategy by joining our discord community by following this invite link or clicking on the Discord logo image. Joining is completely free

![]()